On October 31, 2025, Ukraine’s military intelligence launched a daring operation deep inside Russian territory, targeting the Koltsevoy fuel pipeline near Moscow. The simultaneous explosions severed a vital 400-kilometer corridor that supplied gasoline, diesel, and jet fuel from refineries in Ryazan, Nizhny Novgorod, and Moscow to key Russian military bases.

This marked Ukraine’s deepest strike yet against Russian logistics, disrupting a lifeline that had sustained military operations in eastern Ukraine.

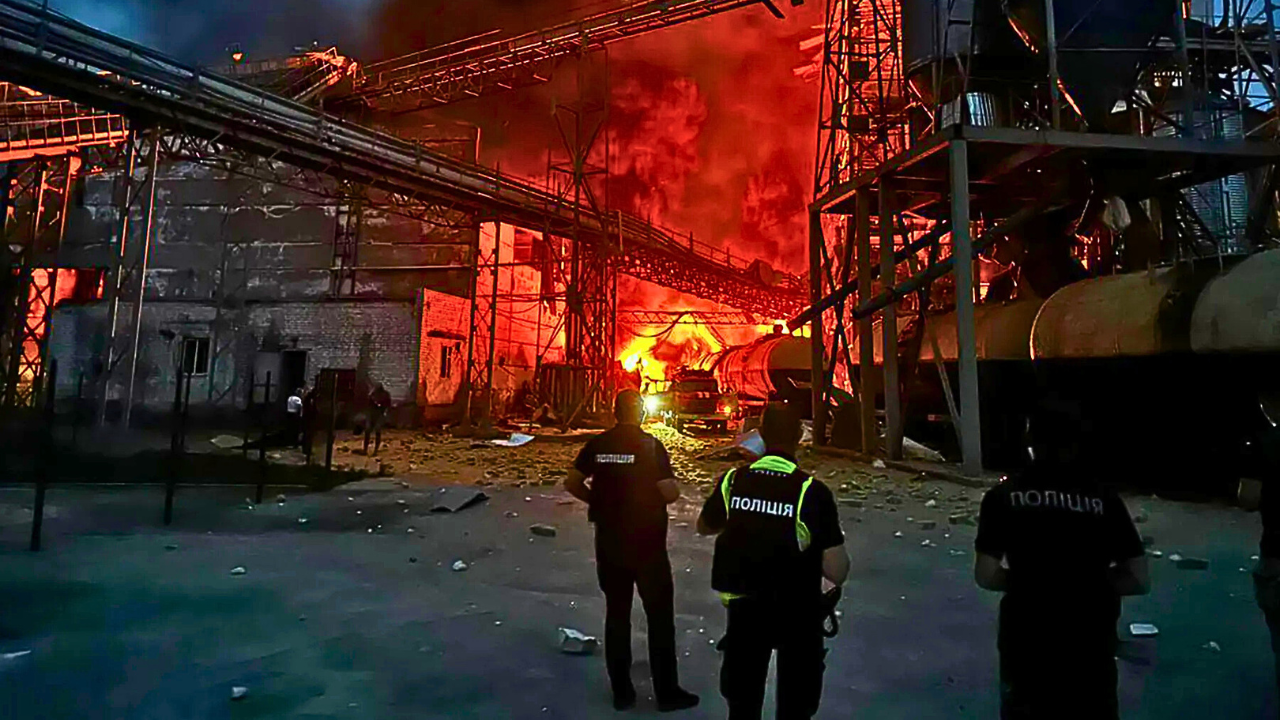

Pipeline Strike: A Blow to Russian Military Supply

The Koltsevoy pipeline was a strategic artery, transporting 7.4 million tons of fuel annually—including 3 million tons of aviation fuel, 2.8 million tons of diesel, and 1.6 million tons of gasoline. Its destruction cut direct supply lines to bases supporting Russia’s campaign in eastern Ukraine.

“This attack has forced us to rethink how we move fuel and supplies,” said a local official in Ramensky district, where the pipeline was hit. The operation required precision and coordination, as all three fuel lines were disabled at once, leaving Russian forces scrambling for alternatives.

Ukraine’s drone campaign, which intensified throughout 2025, has repeatedly targeted Russian energy infrastructure. Independent industry data reviewed by Reuters confirms that at least 16 of Russia’s 38 refineries have been struck since August, temporarily knocking out up to 21 percent of Russia’s refining capacity. Kyiv’s strategy is clear: degrade Russia’s war economy and pressure Moscow into political concessions by systematically attacking energy assets.

Escalating Attacks and Global Ripple Effects

Just two days after the pipeline strike, Ukrainian drones ignited fires at the Tuapse oil terminal on the Black Sea, damaging two foreign civilian ships and forcing a temporary shutdown. The Rosneft-operated port handles about 240,000 barrels of oil daily, much of it destined for China, Malaysia, Singapore, and Turkey. These attacks have contributed to a sharp decline in Russia’s fuel exports.

In September, shipments via Black Sea and Azov Sea ports fell by 23.2 percent from August, while Baltic ports saw a 15 percent drop. Diesel exports from Primorsk, a major Baltic terminal, plunged by 30 percent month-on-month.

The cumulative effect of these disruptions is evident in Russia’s fossil fuel revenues. By September 2025, daily earnings had dropped to €546 million—a 4 percent monthly fall and a 26 percent decline compared to the previous year, according to the International Energy Agency. Export volumes fell 13 percent in a single month, directly impacting Russia’s ability to fund its war effort. “Ukraine’s strikes have dealt a severe blow to Russia’s cash flow and logistics,” said energy economist Dr. Elena Markova.

Domestic Shortages and Kremlin Response

Facing mounting losses, the Kremlin responded by extending its gasoline export ban through the end of 2025 and imposing new restrictions on diesel, marine fuel, and gasoil for non-producers. Prime Minister Mikhail Mishustin signed the order after weeks of refinery damage and growing fuel shortages. Officials described the move as a temporary stabilization measure, but insiders acknowledged it was a defensive reaction to Ukraine’s relentless campaign.

Across Russia, motorists have faced rationing and long queues as supplies dwindled. Pro-Kremlin media reported fuel stations in multiple regions limiting purchases per driver. In Crimea, annexed by Russia in 2014, shortages have become acute. Rural areas, especially in the south, have struggled to secure diesel ahead of winter, with 2.6 percent of retail stations nationwide closing—rising to 14 percent in some southern regions.

“We’re worried about getting through the winter,” said Irina Petrovna, a farmer near Krasnodar. “Diesel is scarce, and prices keep rising.”

International Sanctions and Shifting Energy Markets

The energy war has reverberated far beyond Russia’s borders. In Brussels, the European Commission formally adopted a plan to end Russian gas imports by January 2028, with short-term contracts expiring in 2026 and long-term ones by 2028. Russia’s share of the European gas market has collapsed from 45 percent in 2021 to 18 percent in 2025.

Western nations have escalated sanctions. In October, the United States blacklisted Rosneft and Lukoil, freezing assets and restricting transport. The UK imposed ninety new sanctions targeting Russian oil infrastructure, and the EU closed loopholes that had allowed limited trade in refined fuels. “Our goal is to take Russian oil off the market,” said UK Chancellor Rachel Reeves.

Major buyers in Asia have also begun to step back. Indian refiners prepared to halt purchases from Rosneft and Lukoil to avoid U.S. penalties, while Chinese state-owned firms paused seaborne imports, wary of secondary sanctions. Between 2022 and 2025, China and India accounted for nearly 85 percent of Russia’s crude oil exports. Their caution threatens to remove Moscow’s last reliable energy customers.

Winter’s Uncertain Outlook

As winter approaches, both Russia and Ukraine face the prospect of energy shortages. Russia struggles with domestic supply despite export bans, while Ukraine’s energy ministry warns that up to one-third of natural-gas output could be lost to continued shelling. Aid agencies are preparing for potential blackouts and heating crises on both sides.

The destruction of the Koltsevoy pipeline and the broader energy war have shifted the conflict’s dynamics, directly affecting civilian life and national resilience. With Ukraine’s drone reach expanding, Western sanctions tightening, and Asian buyers hesitating, Russia faces a strategic dilemma: prioritize domestic supply or revive export revenue. The Kremlin has ordered heightened protection of refineries and ports, anticipating further deep-strike operations as the war’s energy front intensifies.