Prices for computer memory are climbing sharply, and a key U.S. supplier is walking away from everyday buyers just as demand from artificial intelligence explodes. Since mid-2025, RAM costs have jumped by 30–100%, and shelves that once held budget-friendly kits are thinning out. As data centers race to secure high-bandwidth memory for AI systems, they are competing directly with home PC builders, small businesses, and families—often winning on price and volume. The result is a quiet but significant shift in who the memory industry is prioritizing.

Crucial’s Legacy and a Highly Concentrated Market

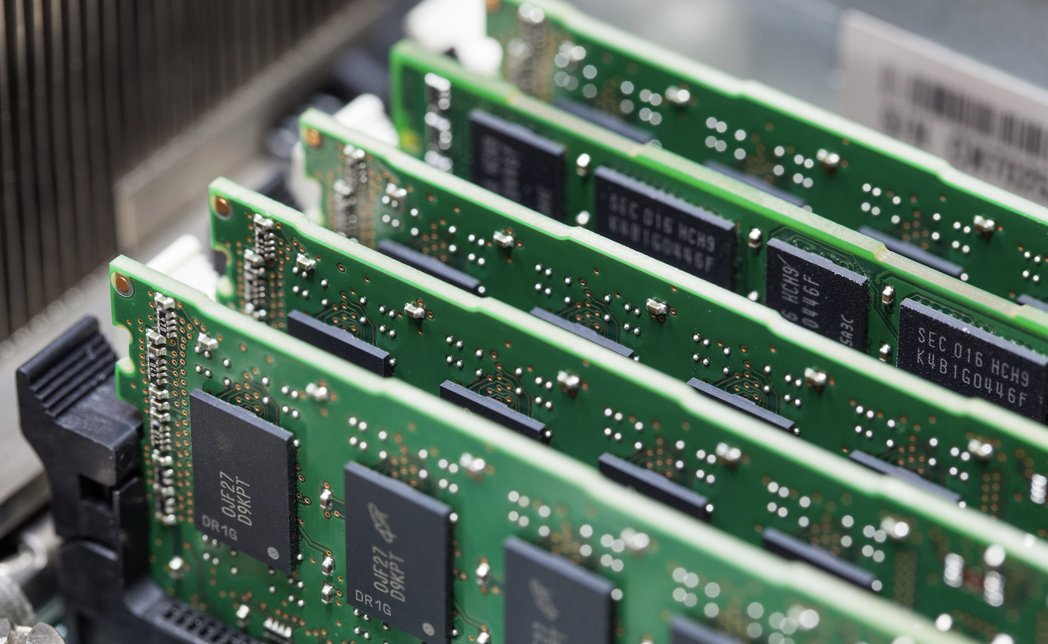

Dynamic random-access memory (DRAM) production is dominated by three companies: Samsung and SK Hynix in South Korea, and Micron in the United States. Samsung and SK Hynix together supply about 70% of the world’s DRAM, while Micron accounts for roughly 25% of global production capacity. That concentration means that strategic moves by any one of these firms can rapidly ripple through consumer, enterprise, and government buyers at the same time.

For nearly 30 years, Micron’s Crucial brand served as one of the most recognizable names in PC upgrades across North America and Europe. Established in September 1996, Crucial built a reputation for reliable, reasonably priced RAM and SSDs that appealed to gamers, DIY enthusiasts, students, and office users alike. As the last major U.S. DRAM producer, Micron helped anchor domestic supply even as other American memory makers disappeared.

The AI Boom Rewrites the Business Case

That long-standing balance began to unravel as demand for AI infrastructure surged in 2024 and 2025. Training and running generative AI models require enormous amounts of high-bandwidth memory, or HBM, which can move data much faster than conventional DRAM. Micron’s HBM revenue reached nearly $2 billion in the August 2025 quarter, implying an annualized rate around $8 billion. Those sales come with higher margins and stronger growth prospects than the consumer RAM market, which has long behaved like a low-margin commodity sector.

Industry forecasts suggest AI-related memory demand will stay elevated through at least 2028. For Micron and its shareholders, the math is straightforward: reallocating manufacturing capacity from budget consumer modules to premium HBM and enterprise products promises far greater returns. As a result, the company has chosen to concentrate on data centers, cloud providers, and other large institutional customers rather than individual PC builders.

Micron Shuts the Door on Consumer Buyers

On December 3, 2025, Micron announced it will fully exit its Crucial-branded consumer business, ending sales of RAM and SSDs through retailers, online stores, and distributors worldwide. Final shipments are scheduled to wrap up by the end of Micron’s fiscal second quarter, around February 2026. From that point, the company’s production will be focused on enterprise and AI customers, marking the end of Crucial’s nearly 30-year run in consumer markets.

Sumit Sadana, Micron’s chief business officer, described the move in stark terms: “Micron has made the difficult decision to exit the Crucial consumer business in order to improve supply and support for our larger, strategic customers in faster-growing segments.” Chief executive Sanjay Mehrotra has framed the shift as a logical response to market realities, arguing that redirecting Micron’s 25% share of global DRAM capacity toward HBM and other enterprise products aligns with long-term growth priorities.

For consumers, the immediate implications are fewer choices and higher prices. With Micron stepping away, effective control of mainstream DRAM for home and office machines consolidates further under Samsung and SK Hynix. Brands such as Corsair and G.Skill will remain on store shelves, but they depend on chips made by the same two manufacturers, increasing pressure on already tight supply. Retailers including Amazon, Newegg, and Best Buy will sell through remaining Crucial inventory over the coming months, after which alternatives may be costlier or harder to find.

Looking Ahead: Scarcity, Policy Questions, and Consumer Fallout

Micron’s exit lands amid an ongoing global semiconductor crunch that began in 2020 and has never fully cleared. Industry leaders report simultaneous shortages in HDDs, DRAM, NAND flash, and advanced HBM, and new fabrication capacity is not expected to meaningfully ease constraints until at least late 2028. During this period, governments, enterprises, and households will compete for limited memory supplies, with institutional buyers generally able to pay more and lock in priority allocation.

Analysts warn that if Samsung and SK Hynix follow Micron’s lead by further tilting output toward AI and data center clients, RAM and SSDs for personal computers could shift from routine purchases to premium products. Estimates from Tom’s Hardware suggest that if current 30–50% price increases in RAM persist through 2028, typical PC builds could see total costs rise by $150–$300 for memory alone. With SSD prices also rising by 50–100% in some segments, overall system costs might climb by $400–$500, pushing many mid-range gaming or work machines beyond the reach of budget-conscious buyers.

The move also raises broader policy and geopolitical questions. Micron is the only major U.S.-based DRAM supplier at a time when the U.S. government is supporting domestic semiconductor manufacturing through the CHIPS and Science Act. Micron has announced a $200 billion investment in U.S. memory production, supported by approximately $6.1 billion in direct government grants. That public backing is now effectively underwriting an enterprise-focused strategy geared toward AI infrastructure, while American consumers grow more reliant on foreign-made memory. In Europe and across Asia, regulators and industry planners are weighing similar concerns about resilience, pricing power, and dependence on a handful of large Asian firms.

Antitrust specialists note that the shrinking field of major DRAM producers could attract scrutiny if remaining players significantly cut consumer supply or raise prices in parallel. Smaller manufacturers, particularly in Taiwan and other parts of Asia, lack the capacity to replace Micron’s share of the market. At the same time, investors have largely rewarded Micron’s pivot: the company’s stock climbed 180% in 2025 on AI optimism, even as the Crucial exit announcement triggered a brief pullback.

Over the next several years, the trajectory of AI spending, the investment decisions of Samsung and SK Hynix, and the pace of new factory construction will together determine whether memory remains a relatively accessible component or becomes a cost barrier for many users. Micron’s decision underscores a larger transition in the semiconductor sector, as manufacturers increasingly design their businesses around institutional buyers and high-value computing rather than mass-market upgrades. For consumers, the stakes are clear: the affordability and availability of basic computing power could hinge on how many other companies choose the same path.

Sources

Micron Technology Official Press Release – “Micron Announces Exit from Crucial Consumer Business” – December 3, 2025

Micron Technology Investor Relations – Earnings Call Transcript – September 2025 –

NIST / U.S. Department of Commerce – “President Trump Secures $200B Investment from Micron Technology in Memory Chip Manufacturing” – June 2025

Silicon Motion CEO Public Statements – Commentary on Global Semiconductor Shortage – December 2025 – (Company press release or investor call)

Transcend Official Announcement – SSD and Memory Cost Increase Statement – December 2025 – (Company press release or public statement)

CNBC – “Micron Stops Selling Memory to Consumers, Demand Spikes From AI Chips” – December 3, 2025

PCMag – “RIP Crucial: Memory Supplier Micron Exits Consumer Market to Chase AI” – December 3, 2025 –

Tom’s Hardware – “Micron is Killing Crucial SSDs and Memory in AI Pivot; Company Refocuses on HBM” – December 2, 2025